Table of Contents

ExperienceInteriors

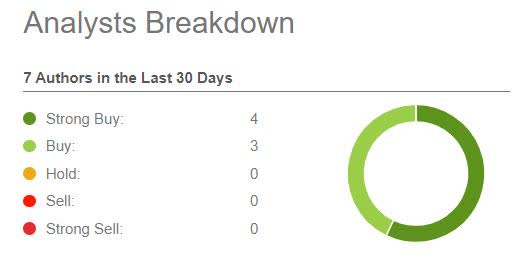

Alexandria Real Estate Equities (NYSE:ARE) is the largest office REIT out there with a market capitalization of ~ $24 billion. It is actively covered and unanimously preferred by Seeking Alpha analysts.

Seeking Alpha

Almost an identical picture can be observed among Wall Street analyst ratings, where in the last 90 day period there have been 6 strong buy, 3 buy and only 1 hold recommendations.

Now, whenever there is this strong consensus, I tend to question whether everything is not already baked into the cake that ultimately diminishes the chances of capturing excess returns. Let’s remember that in order to beat the market one has to allocate towards assets for which the beginning value does not factor in all of the information, which is readily available and obvious for a majority of the financial market participants. Plus, an overly positive view on an asset tends to imply richness in valuations, above what is justified by the fundamentals.

Goal of the article

The key objective is to take a look at certain areas of ARE’s fundamentals and the most common arguments used by bulls, and give different perspectives to challenge the undivided bull thesis. Hopefully, this will broaden the scope of inputs used in evaluating ARE as an investment for both existing and prospective ARE’s shareholders.

Below I will explore three most common arguments that support ARE’s buy thesis, and try to outline some points that weaken these assumptions.

#1 Cheap valuations

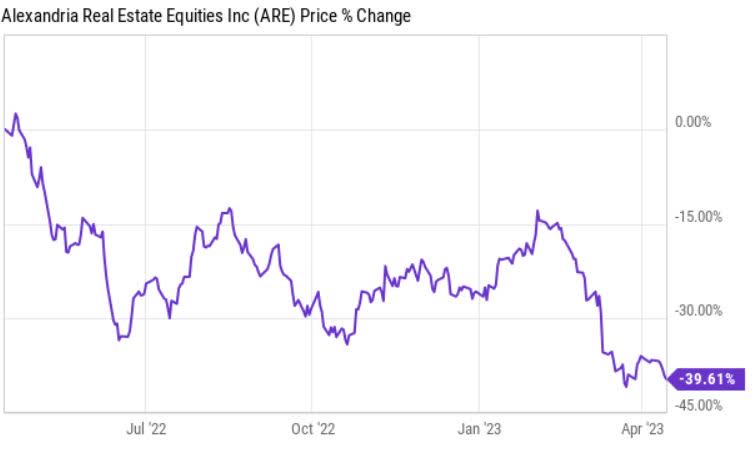

In the past 12 month period, ARE’s share price has suffered a lot together with the rest of the US office REIT segment.

Ycharts

The ~ 40% decline in share price has been much steeper than compared to a broader REIT market. For instance, Vanguard Real Estate ETF (VNQ), which is one of the largest US equity REIT indices representing a diversified basket of various REIT segments has fallen by 22% in a comparable period. This implies a divergence of 18%.

ARE’s bulls are making the argument that this disconnect from the rest of the REIT market is not just and is mostly attributable to the market blending ARE together with other low quality office REITs. Plus, there is a rather popular thesis that even looking at the historical price levels, the ARE’s share price is trading at way too depressed levels, hence some expected gains from mean reversion could be captured.

Here are my counter arguments.

First, on a historical 1 year basis, ARE’s peers have suffered much steeper declines than that of ARE. Namely, the average drop in market cap of total US equity REIT segment has been by 19% larger than for ARE.

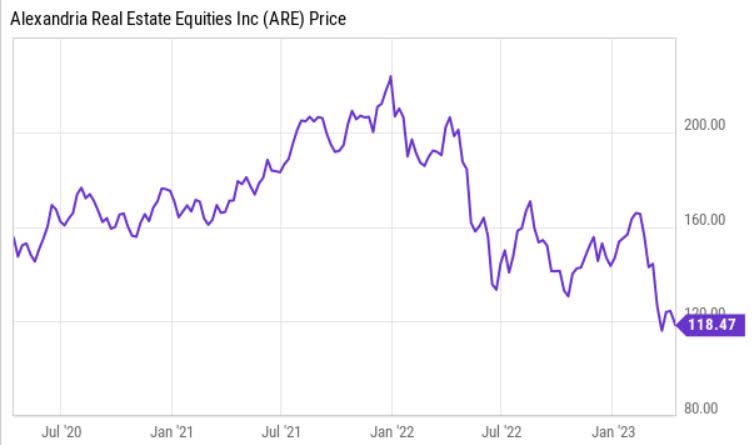

Second, looking at the historical 3 year period, ARE’s share price is not that punished, especially considering that back then the interest rates were much lower (supporting higher valuations per definition).

Ycharts

Third, if we zoom back and take a look at a past 5 year period, the prevailing share price is almost at the same level, unchanged.

Ycharts

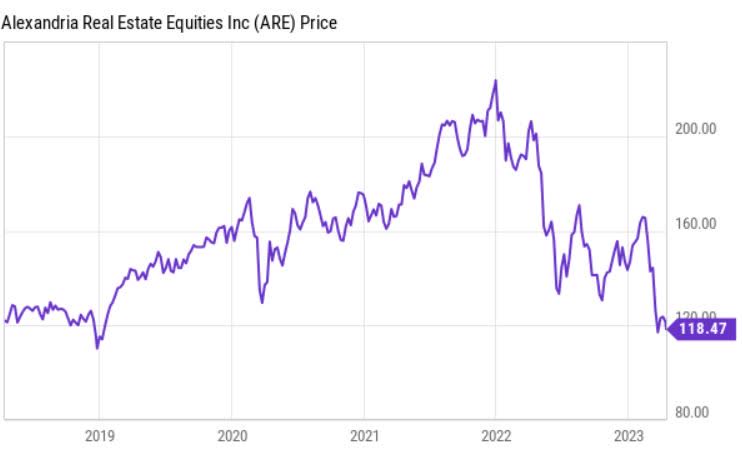

Granted, it is a bit comparing apples with oranges as back then, ARE had less cash generation power than it has now.

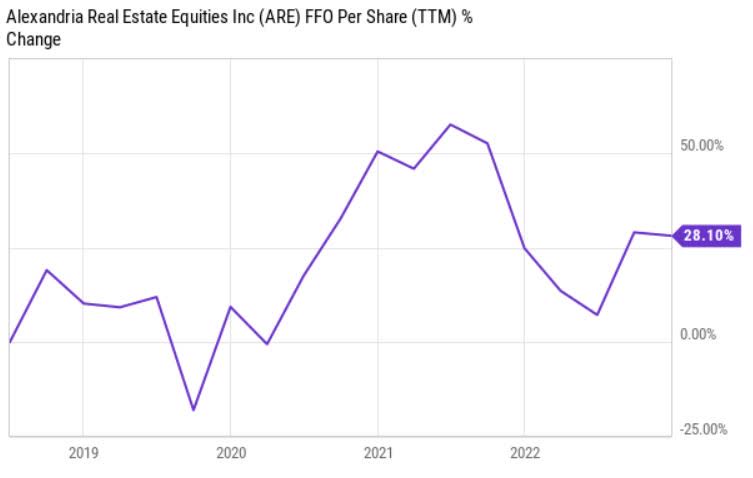

Ycharts

We can see that over the comparable period, ARE’s FFO per share grew by 28%, while as reflected in the previous chart, the share price has plunged back to the level when the ARE had not achieved this kind of cash generation power.

My counter argument for this lies in the interest rates. Back then, we lived in an ultra-low interest rate environment, which supported seriously inflated asset prices. Now we have US 10 year treasury yielding at ~ 3.5% with 2 year rate revolving around even higher levels of ~ 4%. For real estate valuations this is a huge impact as real estate as such from the valuation perspective is treated as something between bonds and equities. Namely, it has a greater exposure to duration risk than standard equities. All this significantly substantiates the fact that the drop in ARE’s share price is logical.

Lastly, to add icing on the cake – ARE trades at much higher price-to-FFO multiple than other US equity REITs. According to the NAREIT database (March, 2023), the implied valuation discount (based on FFO 2023 consensus estimates) of ARE’s peers is roughly 54%. This does not make the bull case stronger.

#2 Fortress balance sheet

It is true that ARE has one of the best balance sheets, not only among office REITs, but also in the context of the entire REIT space. The following are key themes characterizing the financial resiliency:

- Investment grade credit rating of BBB+

- No debt maturities until 2025 and very long weighted average maturity profile of 13.2 years

- Net debt and preferred stock to adjusted EBITDA of ~5x, which is a rather healthy level

In 2023, ARE plans to spend $2.97 billion in CapEx. Given the 2022 FFO payout ratio of 60% and 2023 FFO guidance midpoint of $8.96, ARE is expected to retain ~ $526 million of cash to fund the CapEx plan.

The remaining CapEx funding gap will be closed by a combination of incremental debt and asset disposals. As per ARE’s guidance, the incremental debt is expected to land at $900 million.

These additional debt proceeds will not leave a material impact on the overall financial profile of ARE. However, the freshly issued debt will be subject to the prevailing financing terms, which are less favourable compared to the average cost of debt level that ARE had ending 2022.

At year-end 2022, ARE’s total outstanding debt of $10.5 billion yielded 3.5%. It is safe to assume that this percentage will increase and as a consequence there will be a notable downward pressure on the underlying cash flows.

For instance, the current credit lines are subject to SOFR + ~1%, which implies ~ 5.7% cost of debt. The recent long-term fixed debt issuances are subject to approximately 5% (obviously depending on the duration profile).

Already this year we can expect a notable increase in ARE’s interest expense component stemming from the additional $900 million of debt proceeds. Given that ARE continues the same strategy (i.e., financing CapEx with a mix of fresh debt, divestitures and retained earnings), we can expect further pressure from the growing interest expense component even though the first notable debt due dates start from 2025.

The bottom line is that ARE has and will have a strong capital structure, underpinned by investment grade credit rating. Yet, the weighted average debt maturity profile does not provide protection from surging interest expenses as it might be considered from the distant debt maturity profile. Already this year and most likely until 2025 we will see ARE incurring higher and higher interest expenses, which will make it more challenging to grow the FFO figure.

#3 Growing top line

One of the widely used arguments in favour of ARE’s bull thesis is the seemingly unstoppable like-for-like NOI growth.

The guidance for 2023 articulates a same store NOI growth of 2 to 4%. This is lower than what was achieved in 2022 – 6.6% increase. Obviously, the 2 – 4% NOI growth number is still great, but the fact that the trajectory is becoming less positive is worrisome. The main reasons for this is the strong comp figure, which is difficult to beat, 2022 property divestitures and a combination of less lease expiries in 2023 with higher base of annual rental revenue per RSF.

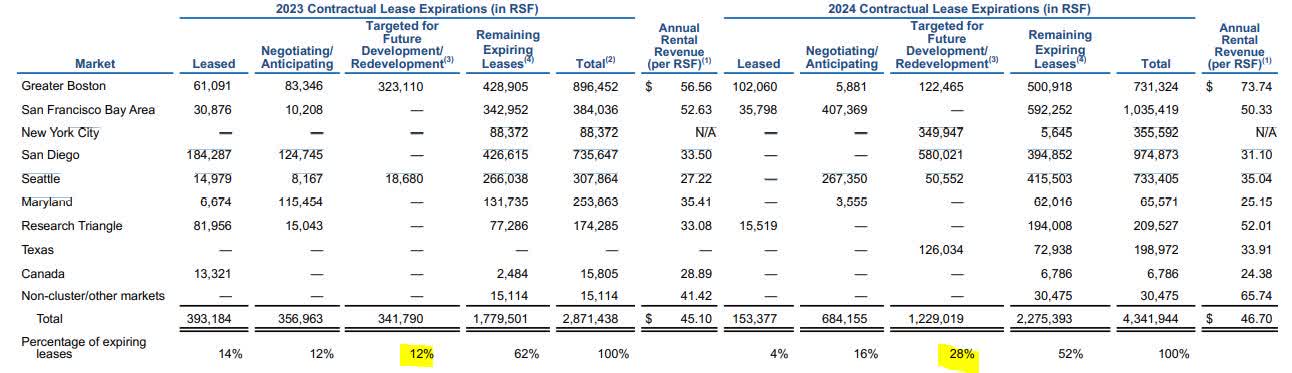

ARE, annual report 2022

Lease expiries in 2023 and especially 2024 (accounting for 18.4% of total leases) will bring some additional headwinds in delivering continuously strong NOI results. From 2023 and 2024 lease expiries, there will be 12% and 28%, respectively, subject to redevelopment activities. Usually, this implies not only an additional need of capital, but also pressure on the occupancy levels. It would be prudent to assume that these redevelopment activities will lead to temporarily reduced NOI flows. Obviously, this will not move a needle, but still make it tougher to beat previous year’s results.

An additional aspect that has to be taken into account when assessing the future NOI is the increased allowances for credit losses. In 2022, ARE tripled its credit (bad debt) allowances compared to the year prior. The amount in absolute terms is rather insignificant amount, a total of $20 million, but it introduces another pattern that is associated with unfavourable rate of change dynamics.

Moreover, I expect that any growth in the NOI will be to a large extent offset by higher interest rate costs stemming from gradual convergence of current ARE’s cost of debt levels to a prevailing rate that is obtainable in the market, on the run. The monetary base value, which is subject to a rate of change in cost of debt is much higher than the one for NOI movement. In other words, an uptick in cost of debt component of a certain percentage embodies more pronounced impact on the FFO than the growth in the NOI figure.

Final thoughts

In my opinion, ARE carries robust fundamentals and is one of the safest if not the safest US office REIT from the financial risk perspective.

However, at the same time I am skeptical that ARE will manage to deliver alpha (above market level returns) as there is a lot of priced in and 2022 closed at very hard-to-beat figures.

Compared to other US office REITs, ARE trades at a significant premium, which is understandable given ARE’s asset quality and tenant profiles. However, it inherently creates tougher ground from which to outperform when the tide turns. The fact that it currently trades way below its historical norm is to a large extent justified by the prevailing interest rate environment and sector-wide headwinds.

In a nutshell, my base case is that ARE will perform in line with the market at the same time fully delivering on its dividend targets. Yet, I would not expect beating the market by going long ARE at these multiples.