Table of Contents

LordHenriVoton

Customer spending on companies jumped by .7% in November from Oct, seasonally adjusted, and by 8.9% from a 12 months ago, according to the Bureau of Economic Evaluation now. Companies accounted for 62.1% of full customer paying out: coverage, health care, housing, vacation bookings, entertainment, repairs, cleansing services, haircuts, etc.

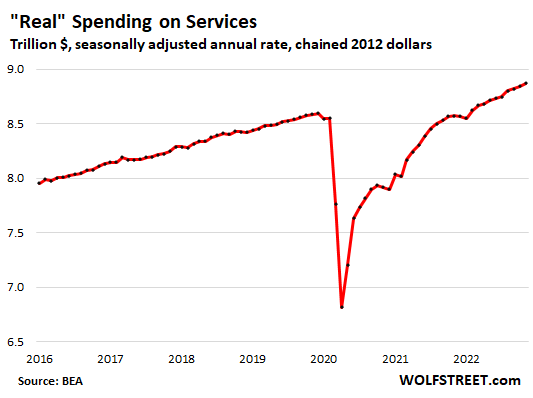

Adjusted for inflation, so “genuine” customer investing on services rose by .3% in November from October, and by 3.5% year-over-year. The very last time prior to the pandemic when authentic shelling out on solutions grew at that year-more than-yr amount was in July 2015. Desire for solutions has been relentlessly potent, irrespective of inflation and regardless of the Fed’s efforts to tighten and therefore lower demand.

Paying out on services has effortlessly outrun inflation that carries on to rage in companies, and so this demand for services carries on to present more fuel for inflation in solutions:

But “authentic” paying on products fizzled

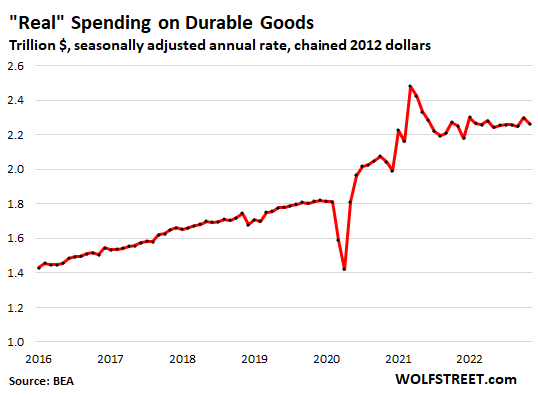

Paying out on durable items, not altered for inflation, plunged by 3.3% in November from October. Long lasting items are new and applied autos, appliances, electronics, furniture, etcetera.

Altered for inflation, “real” shelling out on resilient items fell much less, -1.5% in November from October, because of to the steepest fall in strong goods price ranges in years.

In contrast to a calendar year ago, genuine spending on sturdy merchandise was just about flat (+.6%). Take note the historic stimulus-fueled spike in demand that is now acquiring worked off. In contrast to November 2019, “genuine” expending on tough items was nevertheless up by 25%!

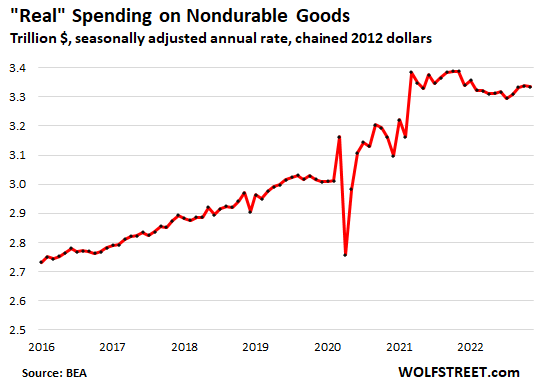

Spending on non-strong products, altered for inflation, dipped by .1% in November from Oct, and was down 1.5% from a yr back. Nondurable merchandise are dominated by food, gas, and house supplies. And it’s even now up by 10% from November 2019:

Total “serious” spending expansion: slowing

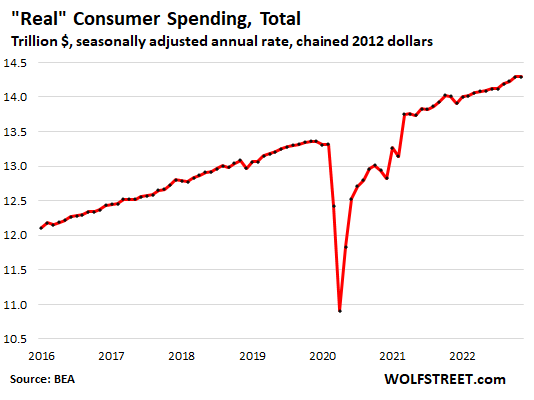

All round buyer expending on merchandise and products and services, not altered for inflation, ticked up .1% for the month, but was nonetheless up by 7.7% year-more than-year.

“Serious” customer shelling out on goods and companies, modified for inflation, was unchanged for the thirty day period and up by only 2.% year-above-12 months.

In the many years in advance of the pandemic likely back again to 2015, real development of client spending of 2% calendar year-about-year happened only in 1 thirty day period. The rest of the months, paying out was significantly higher. To get to the months with 2% expansion and underneath, we have to go back to 2014.

So the Fed’s tightening has had an impression on customer investing, and inflation has had an affect as the temper has soured. But not long ago, it helped that gasoline price ranges have re-plunged. Nothing turns Us residents off much more than acquiring gouged at the pump.

But the slowdown in desire has strike goods, where inflation is already backing off, when expansion in spending on products and services remains robust, and this is of program where by inflation is now solidly entrenched.

Editor’s Observe: The summary bullets for this short article had been picked out by Trying to get Alpha editors.